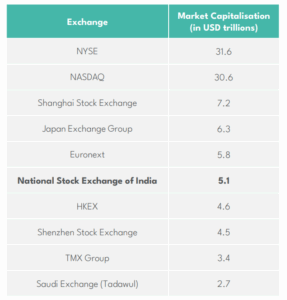

Bombay Stock Exchange – 150-year anniversary

The Bombay Stock Exchange (BSE) in India, Asia’s oldest, celebrated its 150th anniversary on April 17, 2025, marking a century and a half since its 1875 founding by Premchand Roychand. The BSE remains the world’s largest stock exchange by number of listed companies that today exceeds 5,500. This compares to around 1,660 on the London Stock Exchange.

The BSE has a close cousin – the NSE (National Stock Exchange of India), which was founded in 1992. It has stricter listing requirements which results in a smaller but generally more established and actively traded pool of companies. Together the BSE and NSE are home to over 7,500 listed companies.

Emerging retail investor dominance

Since the pandemic, the NSE has added 16 million new investors every single year. As of November 2025, there were more than 130 million unique investors – that’s triple the amount compared to six years ago. Retail investors now hold roughly 19% of the entire NSE’s market cap – the highest in 22 years.

A significant driving force is the popularity of India’s investment vehicle, the Systematic Investment Plan (SIP). What started as a niche financial product in the 1990s, has now matured into a national cultural phenomenon and is the definitive wealth-creation tool for millions of Indian investors.

To highlight this success, monthly contributions reached $3,464 million in November 2025, marking an 11% increase in just nine months. This momentum over time has translated into a colossal ecosystem that now manages over $194 billion in assets, underpinned by a vast and growing network of over 94 million active accounts.

Driving this growth is a significant demographic shift and secular growth in India’s middle class. Nearly 40% of NSE investors are now under the age of 30, a dramatic rise from just 23% in 2019. As the world’s most populous nation with a median age of just 28.4 years, India is benefiting from structural investment flows that is expected to continue support the Indian equity market.

Stock picker’s paradise

India is a ‘stock-picker’s paradise’ due to its massive breadth of 5,500+ listed entities and high liquidity (averaging US$ 10–12 billion daily). Crucially, the low correlation with the U.S. (0.17 vs S&P 500) offers a rare combination of vast, uncorrelated and liquid stock picking opportunities.

Phoenix Mills – retail-led urban development. Phoenix Mills is India’s largest retail-led, mixed-use developer. It has exposure across the entire real estate space, including retail malls, entertainment complexes, commercial spaces, and hospitality. Phoenix’s sustainable competitive advantage is supported by its large, diversified portfolio of prime retail-led assets and strategic long-term partnerships with global high-street brands, which drive superior footfall and industry-leading rental yields. The company benefits from several structural growth drivers such as increasing discretionary spending, rapid urbanisation and a rising middle class. India also benefits from extremely low mall penetration of just 0.5 square feet of retail sales area for grade A malls (which is lower than Indonesia, the Philippines and Vietnam). Its share price is up 317% over the five-year period ending January 2026.

Lemon Tree Hotels – riding India’s hospitality boom. Lemon Tree Hotels is India’s largest hotel chain in the midscale segment. Its success is thanks to an aspirational shift towards branded hotels, aided by secular growth in domestic travel, higher disposable incomes and improving transportation. The investment thesis is driven by a dramatic supply-demand mismatch; as Hilton’s CEO noted, India has fewer total branded hotel rooms than the city of Las Vegas alone. Domestic demand is projected to grow at 9.7%—significantly outstripping a 5.9% supply growth over the next five years. Its share price is up 207% over the five-year period ending January 2026.

Mahindra & Mahindra Financial Services – the Financial Engine of Rural India. M&M Finance is a leading Indian Non-Banking Financial Company (NBFC) that serves as the financial backbone of the Mahindra Group. It caters to the rural mass market with a vast network across the country, reaching over 480,000 villages. The company benefits from two of our themes: a sustainable competitive advantage in its substantial scale and reach, and a monetisable structural growth opportunity where financial services remain in short supply.

Growth opportunities include the “premiumisation” of rural India, where demand is shifting from a value-driven to an aspirational market. For example, individuals moving from a basic motorcycle to an entry-level car. Its share price is up 111% over the five-year period ending January 2026.

Polycab – wired for growth. Polycab is the largest manufacturer of cables and wires in India. This market is highly fragmented, with unorganised, small-scale players holding nearly 35-40% of the market. Stricter quality regulations (like BEE and BIS standards), the implementation of GST (consumption tax), and increasing brand consciousness among consumers have shifted demand toward organised players such as Polycab. The company benefits directly from the government’s massive push in public infrastructure spending. The wire and cable industry is expected to grow at 1.5x to 2x of real GDP growth. Its share price is up 484% over the five-year period ending January 2026.

Capturing this opportunity

We focus on long-term structural growth themes, such as digitisation and domestic consumption, with roughly half of our holdings situated in the under-explored small and mid-cap space. This focus on the ‘hidden’ 5,500+ universe provides us with a differentiated and uncorrelated source of alpha.

We believe the ideal environment for active management requires scale, diversity, and structural tailwinds. That’s the case of the Indian stock market, where you can find a wealth of securities that have the potential to deliver higher returns than the market. Driven by a powerful entrepreneurial surge and a robust economy fuelled by domestic factors, rather than global volatility, India has evolved into one of the most compelling markets globally for active stock selection.

SOURCES:

BSE and NSE, as of 2025, The Economic Times as of 27th December 2025, Bloomberg as of 31st December 2025, Hilton as of January 2026, company data (for Mahindra & Mahindra Financial Services, Polycab and Phoenix Mills, as of 2025).