South Korea – Winds of change or another false dawn?

INTRODUCTION – THE SOUTH KOREAN DISCOUNT & GOVERNANCE

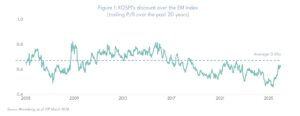

For over two decades, South Korean equities have traded at a persistent discount to Emerging Markets, as can be seen in Figure 1. This is not because of macroeconomic weakness nor because of inferior businesses, but due to the way those businesses are run. The chaebol system – family-controlled conglomerates using opaque cross-shareholding structures to exercise control over assets far exceeding their economic ownership – has produced a corporate culture in which capital allocation decisions are made with one primary beneficiary in mind: the founding family.

WHY RETURNS ON EQUITY REMAIN STRUCTURALLY LOW

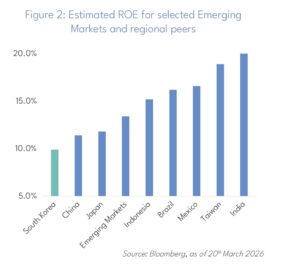

Dividends have been historically suppressed despite strong cash generation, in part because South Korea’s historically high dividend tax rates (up to 49.5% including local income taxes) reduced the appeal of distributions; but also, because low payouts keep valuations depressed, reducing inheritance tax costs when controlling stakes pass between generations. Hoarding cash by controlling shareholders is thus common, despite the stock market’s main constituents generally having strong cash flow generation and robust balance sheets. Moreover, related-party transactions routinely transfer value to family-affiliated entities. The result is a structurally low return on equity that has persisted historically, with a wide gap with peers (as can be seen in Figure 2) and many South Korean equities trading historically below their book value, as has also historically been the case with Japanese equities.

CHAEBOL DYNAMICS & PATTERNS

In our view, one of South Korea’s major consumer companies exemplifies the governance problem. Their product has been a dominant brand for 24 consecutive years, with a 50%+ domestic market share. By most conventional measures, a cash-generative consumer franchise with a brand that has no meaningful competition should be a compelling investment opportunity. However, the stock price has delivered persistently poor returns over the last 15 years. The reason is not that the business is performing poorly; rather, the mechanics of value extraction run through related-party channels: brand royalties paid to the controlling family holding company (in which the family owns a larger stake than in the operating company), related-party supply contracts (e.g. around the packaging) scrutinised by South Korea’s FTC, and intra-group transactions whose terms are opaque and whose primary beneficiary is the controlling family rather than the company’s investors.

Beyond issues with capital allocation and value extraction, South Korean corporate governance has also been marked by a pattern of management misconduct at the highest levels. A leading technology company has seen its founding family face criminal convictions for bribery, with one of its members serving 18 months in prison. A leading automotive company had its founding family investigated for illegal fund transfers and accounting irregularities. According to ISS, approximately 55% of companies with directors who were previously associated with material governance concerns renominated those directors. While this includes financial firms, where the issues often relate to oversight, it also extends to major chaebols. These are not historical footnotes. They reflect a corporate culture in which the interests of the controlling family have, in practice, superseded those of minority shareholders, creditors and stakeholders.

JAPAN’S PLAYBOOK FOR REFORM

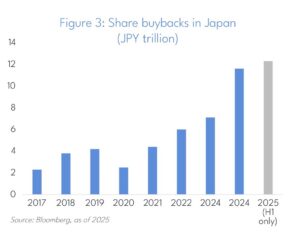

South Korea is not the first market to attempt a governance reset. Japan’s experience is instructive. After decades of similarly depressed valuations and many companies trading below P/B (driven by cross-shareholdings, cash hoarding, low ROE and indifferent management) the Tokyo Stock Exchange introduced mandatory governance disclosure requirements in 2023, effectively requiring companies trading below book value to publish plans to address the gap or explain why they would not. The response was material: buybacks surged, as can be seen in Figure 3, foreign ownership increased and Japanese equities have re-rated sharply. South Korea took note of the Japanese playbook and in 2024 launched reforms, with the aim of unlocking value and enforcing more rigorous governance standards.

THE VALUE-UP PROGRAMME

Launched in February 2024, the Corporate Value-Up Programme is South Korea’s attempt to close the valuation gap with peers. The architecture borrows from the TSE playbook, but with meaningful differences in both mechanism and enforceability, with an emphasis on the programme being voluntary.The key aspect of Korea’s Value-Up is the disclosure pillar, where listed companies are encouraged to publish multi-year plans to improve ROE, capital efficiency, and shareholder returns. The framework follows a “comply or explain” model: firms must state in their governance reports whether a “Value-Up” plan exists. However, we believe that material challenges remain, as the voluntary nature of the programme could produce uneven adoption across South Korean corporates.

The more structurally significant reforms came through subsequent amendments to the Korean Commercial Code. In July 2025, South Korea’s parliament amended the Code to extend directors’ duty of loyalty (previously owed to the company alone) explicitly to shareholders. A further amendment passed in August 2025 introduced mandatory cumulative voting for listed companies with assets above $1.4bn and required that at least two audit committee members be elected independently of the broader board. Both measures address a common concern: the historical tendency for controlling shareholders to appoint boards that may lack real independence. The fact that government intervention was necessary to establish an independent audit committee as late as 2025, illustrates the depth of the governance gap that has prevailed in South Korea.

Reform has continued in 2026, with legislators passing a further revision to the Commercial Act requiring companies to cancel their treasury shares within one year of acquisition (excluding for employee compensation reasons). This is meaningful given that many South Korean business groups have long been criticised for using treasury shares to consolidate their control. Again, as with the audit committee, the fact that mandatory cancellation had to be legislated rather than being standard practice among corporates reveals a lot about South Korean governance standards.

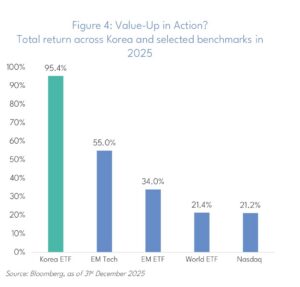

As a result of the above, and as can be seen in Figure 4, the Korean stock market has seen stronger foreign participation and delivered exceptional returns, with a 95.4% rise in the Korean ETF in US Dollar terms in 2025, albeit supported by an additional cyclical tailwind: namely significant AI-related demand for semi-conductors where Korea is a world leader.

REALITY CHECK – WHAT HAS REALLY CHANGED?

Since 2024, share buybacks in South Korea have surged. According to ISS, listed companies repurchased a record USD 12.6bn shares in 2024; more than double than the previous year, and the highest level since the Korea Exchange began tracking the data in 2009. This trend includes some major names, for example Hyundai Motor recently announced a USD 720 million buyback. Our holding, Meritz Financial, became the first Korean financial group to commit over 50% of net profit to shareholder returns through dividends and buybacks. Share cancellations are also gaining momentum; for instance, SK Group (one of the largest chaebols) recently announced the cancellation of treasury shares representing nearly 20% of their free float.

However, board independence in South Korea still remains largely cosmetic in our view. As per ISS, as of June 2025 over 75% of major listed companies still combined the roles of board chair and CEO. In addition, according to Glass Lewis, chaebols such as Samsung, Hyundai and LG recorded no dissenting votes from independent directors between 2019 and 2024. Meanwhile, 70% of outside directors come from academia, government or legal backgrounds rather than a relevant corporate background.

For example, Samsung Electronics currently has 5 independent directors out of 8 total board members (63% independent) which superficially seems positive. However, differences become starker when comparing with peer TSMC. TSMC’s board consists of 10 members, of whom 7 are independent directors (70%), but the key difference is that TSMC’s independent directors include a former CEO of British Telecom, a former chairman of Applied Materials, a former CEO of Xilinx and the former CEO of Xerox. On the other hand, Samsung Electronics’ independent directors are predominantly drawn from Korean academia; with his Chairman being a former Ministry of Economy official and the ex-Financial Services Commission chairman.

E&S: THE SILENT PARTS IN ESG IN SOUTH KOREA

The governance dimension of the reform has attracted the most attention, but we must also consider the E&S of ESG.

The timeline on mandatory sustainability disclosure in Korea has been repeatedly revised. The original FSC plan, initially announced in January 2021, envisioned phased mandatory ESG disclosure requirements applying first to large KOSPI-listed companies, and expanding to all companies by 2030. However, sustainability disclosures in Korea are still not yet mandatory. The FSC has proposed a start date for climate-related reporting for large companies (those with assets over $20bn), with the consultation period running until 31st March 2026, after which the roadmap will be finalised. Moreover, in terms of scope, climate is the only mandatory part of disclosures; everything else is optional. Critically, even within this limited reform, Scope 3 emissions will not initially be mandatory, despite their particular significance in the Korean context given the sectoral composition of KOSPI; with petrochemicals, steel, semiconductors, automotive and shipbuilding dominating the index.

This represents a significant contrast with India, who would perhaps be expected to be less advanced in this area. India’s market regulator (SEBI) introduced sustainability requirements in May 2021, mandating comprehensive ESG data reporting for the country’s top 1,000 companies; beginning in FY23 for the largest 150 companies and from FY26 for the rest. Later, in 2023, SEBI added several Key Performance Indicators covering measurable climate and social metrics (including absolute and intensity-based GHG emissions, renewable energy share, water use, and gender diversity).

Moreover, we believe that the Social pillar is a particularly weak area for South Korean companies. The chaebol system creates complex subcontractor networks where labour conditions, safety and accountability are hard to track and enforce. At the same time, a split labour market (between secure employees in large groups and more precarious subcontracted or temporary workers) means the biggest social risks often sit outside the limited and voluntary reporting scope of companies.

This is not just a data or disclosure gap; it is an accountability gap. For example, as reported by Reuters, in May 2020 the Indian operations of one of the largest South Korean chemical companies suffered a catastrophic styrene vapor leak at their plant in Andhra Pradesh, releasing over 800 tonnes of styrene gas. The accident claimed 23 lives and over 20,000 people were exposed to this toxic gas. An investigation by the Indian government found that 20 out of 21 the factors contributing to the accident were due to mismanagement by the firm’s executives, with alarm systems not working, inadequate safety procedures, and the company operating the plant without federal environmental clearance since 1997.

THE ALQUITY APPROACH

For us, our KPIs are not just “compliance” metrics. We believe that these are indicators of improved alignment between management and shareholders. In the South Korean context, we believe that voluntary disclosure above and beyond regulatory minimums provides a distinct signal. A company that discloses comprehensively (particularly on climate, supply chain, and board accountability) before it is legally required to do so is, in our view, signaling a willingness to be held accountable by a broader stakeholder set. We believe that points to governance that is closer to global standards.

For example, our holding SK Hynix was the first in the South Korean semiconductor industry to issue a sustainability-linked bond with a coupon tied to Scope 1 and 2 emissions reduction targets that were based on output (and not revenue).

Our integrated ESG approach has, in our view, helped us avoid a category of risks; namely the kind of operational, reputational and legal issues that tend to materialise slowly and then very suddenly, impairing the business and shareholder returns.

CONCLUSION

South Korea’s reform agenda is a step in the right direction, but it is not a clean break from the past nor a panacea to ensure future exemplary behaviour. The Value-Up programme has improved the conversation around capital allocation, shareholder returns and transparency enhancements, and some companies are responding with buybacks and more willingness to engage with investors. But that’s only part of the picture. The bigger question (whether corporate behaviour has really moved away from endemic corruption and the opacity and self-interest of chaebol structures) remains open in our view. Because the framework is voluntary and family control persists, progress is likely to be uneven and sometimes, just superficial.

Despite ongoing talk of South Korea being upgraded to Developed Market status, and recent exceptional stock market performance, we still believe that Korea lags many Emerging Markets on essential issues, such as basic disclosure around E&S, treatment of minority shareholders and board independency. A culture of cronyism will not change overnight.

For long-term investors, we believe selectivity remains critical. Rather than assuming the Korea discount will fully disappear, we believe that the opportunity lies in identifying companies where governance reforms translate into genuine accountability improvements and where better transparency across governance, environmental and social practices signals a real reduction in conflict of interests and mitigation of ESG risks. A rising tide does not lift all boats equally.