The Indian rupee experienced a volatile 2025, depreciating by 4.8%, 15.7% and 11.3% against the US dollar, euro and pound respectively. Historically, a depreciating rupee (as with most emerging market currencies) against major pairs such as the dollar or euro is not unusual; for example, rupee depreciation vis-à-vis the dollar has averaged around 3% per year.

Importantly, a controlled depreciation can offer key advantages for an emerging economy such as India, supporting export competitiveness and discouraging excessive imports, thereby encouraging domestic import substitution and strengthening resilience to external shocks. However, an overly sharp depreciation could inflate the cost of essential imports, necessitate costly FX market intervention and prompt higher interest rates to defend the currency.

In our view, the rupee’s weakness in 2025 was driven by transitory factors, including foreign equity outflows and stalled trade negotiations with the US. The FX market appears to be overlooking the structural India is undergoing, as we outline below, which should result in reduced pressure on the currency both in the short and medium term.

India is a trade-deficit country, although this is largely (but not entirely) offset by a substantial services surplus ($188.6 billion in FY25), driven predominantly by IT services. Furthermore, India’s share of global trade has been steadily increasing, as illustrated in Figure 2.

India’s export footprint is firmly oriented towards Western markets, with exports to Europe ($98.4 billion) and the US ($86.5 billion) now dwarfing those to China ($14.3 billion). This is supported by a diversified goods export basket, led by petroleum products (14.5% of FY25 exports), telecom instruments (6%), and pharmaceuticals (5.5%) as shown in Figure 3.

Imports remain primarily linked to energy and gold: crude oil accounts for 19.9% of FY25 imports, gold for 8.1%, and coal for 4.3% as shown in Figure 4.

Despite India’s historic dependence on imported hydrocarbons, a structural transformation is now underway. In a milestone achievement aligned with COP26 objectives, 50% of India’s installed power generation capacity was sourced from non-fossil fuels in June 2025, reaching its Paris Agreement (NDC) target five years ahead of the 2030 schedule. India is therefore reducing its exposure to the volatility of fossil fuel imports and moving towards greater energy self-sufficiency, materially lowering its import burden. This is supportive of the rupee over the medium term.

In January 2026, India concluded a landmark free trade agreement with the EU, representing a transformational opportunity for the economy. The deal creates a unified market of nearly two billion people and a combined economic size of approximately $27 trillion. It is expected to act as a catalyst for growth, with both sides targeting a $200 billion bilateral trade milestone by 2030, fundamentally reshaping flows of goods, services and investment between the two regions.

In addition, coming just one week after the historic India-EU Free Trade Agreement, the long-awaited India-US trade deal was finally concluded. In a swift reversal of events, the US agreed to lower reciprocal tariffs on Indian imports from 25% to 18% while completely removing the 25% punitive levy related to India’s Russian oil purchases. This thirty-two-percentage point reduction significantly bolsters the competitiveness of Indian exports and effectively removes the uncertainty that was weighting on investor sentiment. By removing this headwind, the agreement is poised to transforms the outlook for export-oriented sectors and should act as a trigger for renewed foreign capital flows. These agreements, and following smaller recent deals with the UK and other countries, should further strengthen the rupee’s long-term outlook, particularly given India’s existing trade surplus with the EU (approximately $15.2 billion).

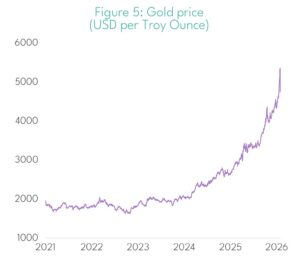

India’s cultural affinity for gold has resulted in an estimated $3.8 trillion of household gold ownership – equivalent to around 89% of national GDP and nearly four times the official reserves of the United States. While gold’s sharp price appreciation has boosted household wealth, it has also intensified macroeconomic pressures: gold imports grew by 27.4% year on year in FY25, accounting for 8.1% of total imports, up from 6.7% in FY24.

Despite this headwind to the current account, a structural rotation is underway as the economy continues to financialise. Equity allocations rose to a record 15.1% in FY25, nearly doubling from 8.7% just a year earlier. While gold remains a cultural investment staple, we expect its share of overall household savings to gradually decline as equity participation continues to rise.

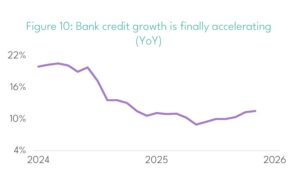

India runs a current account deficit, which is financed through foreign capital inflows. Recently, India’s sovereign debt market entered a new phase of global integration following its inclusion in J.P. Morgan’s Emerging Market Bond Index in 2024 and a planned inclusion in Bloomberg’s flagship Global Aggregate Bond Index in 2026. This has boosted foreign participation in the debt market, with overseas holdings of Indian sovereign debt rising from $20.1 billion in September 2023 to $42.8 billion today.

Despite this, foreign equity flows have recently turned negative. As illustrated in Figure 6, in 2025 foreign institutional investors (FIIs) recorded their largest annual equity outflows on record, totalling $18.8 billion. In our view, this largely reflected “hot money” rotating towards AI beneficiary markets such as China, the US, Korea and Taiwan. These capital outflows were further exacerbated by a slowdown in trade negotiations with the US, followed by an increase in US tariffs on Indian imports to 50%.

In response to rupee depreciation, the Reserve Bank of India (RBI) has adopted a largely measured approach to currency management, rather than aggressively deploying India’s substantial foreign exchange reserves of approximately $700 billion.

India’s long-term export outlook has been materially strengthened in recent years by a combination of structural reforms and targeted industrial policy. In November, the government announced sweeping, long-awaited labour code reforms, consolidating twenty-nine existing laws into just four and creating a far more flexible and formal legislative environment. These reforms have reinforced the 2020 Production Linked Incentive (PLI) scheme – a cornerstone of the ‘Make in India’ initiative launched in 2014 – designed to position India as a global manufacturing hub through targeted subsidies and export support.

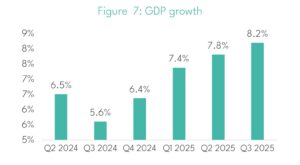

The effectiveness of this approach is reflected in India’s eightfold increase in electronics exports over the past decade. Export momentum is further supported by an accelerating domestic growth backdrop: Q3 GDP growth of 8.2% significantly exceeded consensus expectations, with FY26 projections now positioning India as the world’s fastest-growing major economy for a fourth consecutive year.

The narrowing valuation premium relative to emerging market peers, alongside multi-year low inflation and accelerating economic growth, creates an attractive environment for capital inflows. In our view, this should support a reversal of the rupee’s accelerated depreciation trend observed in 2025.

Despite the volatility experienced in 2025 – which we attribute to transitory trade frictions and capital outflows – India’s underlying structural growth momentum remains intact. India’s transition towards renewable energy, landmark trade agreements such as the EU–India/US India FTAs, and manufacturing reforms under the PLI scheme are collectively strengthening the country’s long-term trade balance.

Coupled with India’s position as the world’s fastest-growing major economy and increasing bond market integration, we expect foreign capital flows to improve. Consequently, we anticipate rupee depreciation to stabilise towards historical norms as the year progresses.

SOURCES:

Deutsche Bank Research & HSBC (January 2026) for Figures 1, 2, and 3; Bloomberg, Morgan Stanley (January 2026) for Figure 6; Motilal Oswal and Goldman Sachs (January 2026) for Figures 7, 8, 9 and 10; Jefferies (28 January 2026); Times of India, “India’s love for gold” (October 2025); Google Finance (as of 30th January 2026) for Figure 5; Government of India (2025); Nirmal Bang, Beyond Market Issue 235 (2025).

India covers more than 3.2 million sq. km and, home to 1.46 billion people,

Read MoreFrom V-Mart’s Lalit Agarwal, who turned a family tailor shop into a 500-store fashion

Read MoreIt’s one of the biggest economies in the world, has one of the strongest

Read More