At Alquity, we believe that true sustainability requires being rational and evidence based whilst maintaining core values. For vast populations in the developing world, the alternative to cement is not a greener life, but a precarious one; vulnerable to extreme weather and lacking basic sanitation. We must ensure that the drive toward net zero is sustained in such a way that millions are not inadvertently condemned to inadequate living conditions. India serves as a prime example of an economy where the context is important to understand and reflect in investment decisions.

According to the most recent National Family Health Survey (2019-2021), nearly 40% of rural Indian households resided in “semi-permanent” or “kutcha” structures (houses made of mud, straw and unburnt brick that frequently wash away in the monsoon). In the cities, the situation is equally critical; Knight Frank estimates point to an urban housing shortage of nearly 10 million units, forcing families into informal slums.

Furthermore, according to Government estimates, the country faces a $1.4 trillion infrastructure deficit to provide basic connectivity, hospitals and sanitation.

Even the energy transition relies on this material; a single onshore wind turbine (3 MW) typically requires roughly 800 tonnes of concrete for its foundation. However, recognising that cement is essential does not mean we accept a blank check for pollution. Because sustainability is paramount, we ensure that high-risk sectors like cement are subject to our most stringent ESG standards.

Furthermore, the wider industry is materially less polluting than it was a decade ago. This is the result of a combination of technological advances, stronger ethical and environmental awareness (at the company, shareholder, and country level), and rational self-interest.

Within the Alquity India Fund, our cement holding is UltraTech, which we believe exemplifies regional best practice within the industry. We also invest in housing finance companies (such as Aptus Value Housing Finance) to support and capture growth in this area, in line with SDG 11 (sustainable cities and communities) and SDG 6 (sanitation). We consciously prefer UltraTech to pure construction companies – as it allows us to support essential infrastructure and housing development while avoiding the significantly higher risks of bribery and conflicts of interest often inherent in the construction bidding and tendering process.

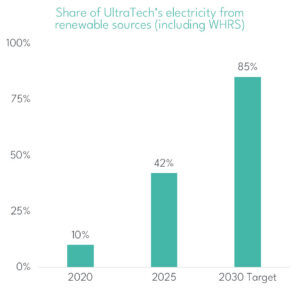

Firstly, it is important to note that UltraTech is aiming to decouple cement production from coal. Cement manufacturing is an energy-intensive process, and hence electricity consumption is significant. UltraTech has committed to sourcing 85% of its total electricity from green sources by 2030 (up from 42% today and from just 10% five years ago). This is not only about reducing emissions in line with the company’s ambitious targets (UltraTech aims to reduce Scope 2 emissions by a further 75% over the next six years); it is also about unit economics.

Grid and coal-based power often cost the company ~INR7.0 per unit whereas power generated from UltraTech’s Waste Heat Recovery Systems (which capture exhaust heat from kilns to drive turbines) costs roughly INR0.8 per unit and generate zero incremental emissions. Solar power costs around INR4.6 per unit. Every percentage point of electricity shifted from grid or coal-based sources to internal green generation directly expands EBITDA margins (up to 200 bps by 2030 assuming the cost of grid power remains the same). With over 1 GW of green capacity currently being deployed (and expected to be doubled by the end of the decade), and approximately one-third of annual capex allocated to new WHRS installations to improve efficiency and cut emissions, UltraTech is building a structural cost advantage that Indian peers still reliant on the coal-heavy grid cannot replicate.

Beyond electricity, a frequently misunderstood value and decarbonisation driver in the sector relates to clinker. Clinker is the high-carbon, high-cost input produced in kilns, and “greening” cement largely means reducing clinker content by substituting alternatives such as fly ash or slag. UltraTech currently operates at a clinker conversion ratio of 1.48x, meaning one tonne of clinker produces 1.48 tonnes of cement, with a target of 1.60x or higher. Achieving this would allow the company to produce roughly 8% more cement without constructing a single new kiln. Given that a new kiln costs over $150 million and takes around three years to build, improving the clinker factor effectively creates “free” added capacity (reducing CapEx requirements), and lowers carbon intensity by roughly 10%.

India’s thermal (coal) power plants generate approximately 340m tonnes of fly ash each year as per India’s Central Electricity Authority. Historically, much of this ash was dumped in ash ponds, which are estimated to occupy over 40,000 hectares of land nationwide. Each tonne of fly ash used in cement permanently encapsulates waste that would otherwise contaminate groundwater. An additional, often overlooked benefit is that fly ash can improve concrete performance in many applications, extending the lifespan of infrastructure such as bridges and hence, reducing long-term emissions. Financially, fly ash is significantly cheaper than manufactured clinker, lowering the variable cost per bag while reducing Scope 1 carbon intensity by a further 7.5%+ if the medium-target ratio of the company is achieved.

Another pillar of the environmental improvements in the sector is the Thermal Substitution Rate (TSR): the ability to replace coal or petcoke with waste being used as an alternative fuel (e.g. plastic, agricultural waste or municipal waste). While global leaders operate kilns with over 50% waste substitution, Indian producers have historically relied on coal, largely due to supply-chain challenges and very poor waste segregation compared with Europe. UltraTech has been aggressively scaling its TSR over the past decade and spent approximately INR4.6 billion last year on CapEx for these initiatives. In the Indian context, given the lack of recycling and proper disposal systems, we believe this is a net positive outcome. While burning plastic generates carbon emissions, it is less carbon-intensive than coal and materially better than the alternative, as plastic pollution is a severe issue in India. If not burnt (or recycled), waste plastic would find its way in rivers and oceans, sit in landfills where it degrades into microplastics and contaminates groundwater, or be openly burned (a common practice in the country) which releases toxic black smoke. By contrast, processing and burning plastic in UltraTech’s kilns significantly mitigates the release of harmful toxins such as dioxins and furans.

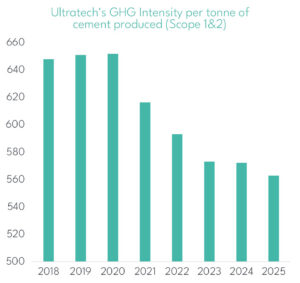

UltraTech’s Scope 1 emissions of 549 kg CO2/t outperforms the global average (600–635 kg/t) and are almost on par with global giants Holcim (543 kg/t) and Heidelberg (534 kg/t). Crucially, UltraTech has achieved this parity largely through product efficiency rather than fuel switching. While peers rely on a TSR of 50%+ in Europe to drive down emissions, UltraTech operates at just a 6% TSR. When including Scope 2 emissions (approx. 13 kg CO2/t), UltraTech continues to demonstrate industry-leading efficiency, compared to the global cement average Scope 2 intensity of approximately 35–40 kg CO2/t and placing it on par with global leaders like Heidelberg.

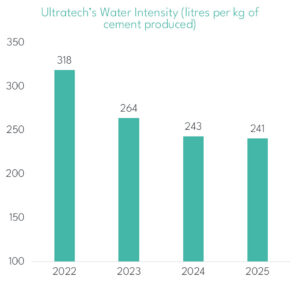

The company’s stewardship and operational resilience also extend to water, a resource under acute stress across the Subcontinent and one we actively monitor and engage actively with our holdings about. While cement is typically a net consumer of water, UltraTech has engineered its operations to give back significantly more than it takes, achieving water positivity of approximately 5x. In FY25, the company harvested over 110 million kilolitres.

For example, in Madhya Pradesh (a region that was water-scarce a decade ago) UltraTech did not simply drill wells, but constructed 67 water-harvesting structures and check dams. Today, water tables have risen sufficiently for local farmers to shift from subsistence farming to higher-value crops such as garlic and chia seeds. Biodiversity has also progressively recovered, with certain species (birds) returning to the area.

As we can see on the chart below, over the past four years, the company’s water intensity has declined over 24%.

Whilst cement has always been critical for India’s development, the environmental impact has dramatically diminished over recent years. We view this as a significant change. With Ultratech, we are backing a management team that views sustainability not as a compliance exercise or box-ticking exercise, but as both a necessity and the primary lever of operational efficiency.

SOURCES:

UltraTech, data as of Q2 FY26; Holcim and HeidelbergCement, latest available data based on 2024 Annual Reports; GCCA, IEA, WRI, Global Averages, as of 2024; National Renewable Energy Laboratory, wind energy cement estimates as of May 2023; CEA, report on fly ash generation and utilisation in thermal power stations as of FY25; Ministry of Health and Family Welfare, national family health survey as of FY2; Knight Frank India demand-supply assessment as of December 2024.

India covers more than 3.2 million sq. km and, home to 1.46 billion people,

Read MoreFrom V-Mart’s Lalit Agarwal, who turned a family tailor shop into a 500-store fashion

Read MoreIt’s one of the biggest economies in the world, has one of the strongest

Read More